Shoppers’ reprioritized sense of self care leads to a rise in DIY pet grooming

Personal pet care enters the spotlight

When hair and nail salons temporarily closed their doors during shelter-in-place ordinances earlier this year, Americans looking to maintain their personal care routines had little choice but to adopt a do-it-yourself (DIY) approach to beauty and self-care. But this trend didn’t stop at the human consumer level: As shoppers became more invested in their DIY routines, many pet owners placed added importance on maintaining their pet’s health and hygiene at home, especially when temporary (and some permanent) business closures left consumers with few other options.

More than 11 million U.S. households adopted a pet during the pandemic, according to the American Pet Products Association’s (APPA’s) “COVID-19 Pulse” study. This sparked notable sales growth across all pet care categories (i.e., pet supplies, pet food and pet treatments). Pet supplies have been the fastest-growing category in pet care throughout the pandemic and pet grooming has been one of the fastest growing segments within the category.

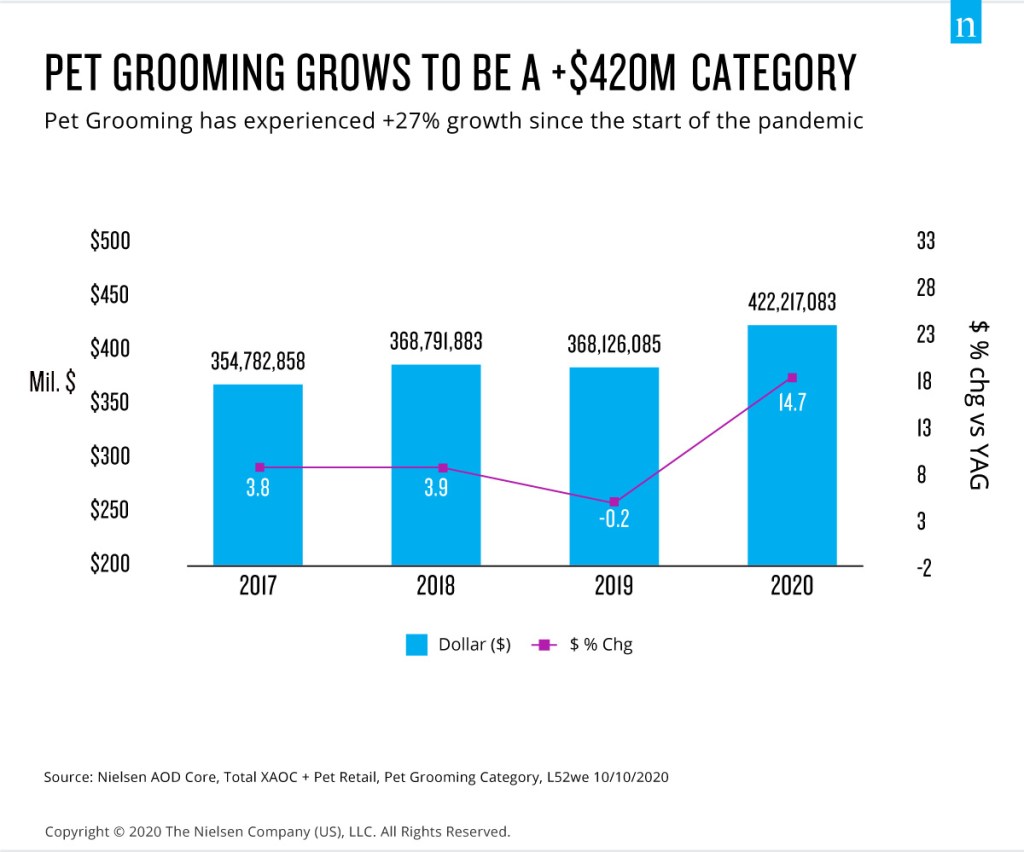

In tune with consumers’ recently developed DIY health and beauty habits, pet parents haven’t limited their efforts to themselves, as many have familiarized themselves with at-home pet grooming this year. While the sales growth rates for grooming necessities like brushes and combs, grooming supplies, shampoo, and conditioner have slowed since the peak purchasing period back in May, sales remain substantially above pre-COVID levels, with total pet grooming sales up 27.4% since the outset of the pandemic. This far outpaces the 3.2% growth generated by the total pet care category.

As shoppers stocked up on what was newly deemed essential, increases in the average number of units purchased per shopping occasion and average spend per buyer contributed to pet grooming category growth. In addition to driving increased grooming sales, the pandemic boosted household penetration by 5.1% across all NielsenIQ tracked channels during the 52 weeks ended Oct. 31, 2020.

But there’s still a massive opportunity for retailers and brands to capture new buyers. According to the APPA’s 2019-2020 National Pet Owners Survey, over 106 million households own a cat or dog, but NielsenIQ Homescan data shows that only 12.3 million households purchased pet grooming products in the year ended Oct. 31, 2020. To drive increased adoption, brands need to educate consumers on the importance of personal pet care with comprehensive deliverables that inform shoppers on how to maintain their pet’s health. By offering pet-friendly products that make clear connections between consumers’ reprioritized sense of self-care and pet personal care, brands and retailers will be able to tap into the large segment of households that have yet to purchase within the pet grooming category.

Online captures the majority of pet grooming purchases

Pet care products had strikingly high omnichannel adoption rates before the pandemic. However, as COVID-19 pushed more than 18 million Americans toward the online CPG landscape for the first time, e-commerce accounted for more than half (53%) of all pet grooming dollar sales between April and September 2020, up 11 percentage points compared with pre-COVID levels. Within this 53% figure, roughly 5% of e-commerce purchases were fulfilled via click-and-collect, but click-and-collect sales heavily declined after the peak pandemic purchasing period in May. By offering exclusive in-store savings, special click-and-collect promotions, in-store product education and contactless payment and pickup methods, retailers can entice online shoppers to visit brick-and-mortar stores and convert additional sales.

Pet grooming shoppers will become further entrenched in their online shopping habits into the ‘new normal’ and e-tailers need to enhance their customers’ shopping experience through easy-to-use personalization tools as consumers continue to seek out convenience. While pet shoppers continue to shift toward the omnichannel landscape, retailers need to create comparable experiences both in-store and online by providing diverse product assortments, offering promotional sales and price points to accommodate different budgets and educate consumers on pet personal care needs. Retailers should focus on their omnichannel capabilities and make products available through multiple vehicles like home delivery, subscription services, click-and-collect and curbside pickup—all of which will become even more appealing amid rising COVID-19 cases.

Personal care brands are offsetting losses through pet product lines

The total pet grooming category has consistently seen substantial growth throughout the pandemic, and private label brands continue to dominate as much as 75% of total dollar share in some subcategories. Given the lack of diversity in products and brands, consumers looking to cater to their pets at home are limited in terms of innovation, and it’s possible that not all shoppers’ needs are being met.

More human-centric personal care brands are entering the pet grooming space, with Hempz, Wet Brush, and Waterpik all releasing successful pet product crossovers. Many of the top pet grooming brands got their start in human beauty and personal care, including Burt’s Bees and CHI, and these brands have experienced highly accelerated growth as consumers stocked up on at-home pet care. Outside of the health and beauty care space, tool manufacturer Dremel has expanded its expertise into pet grooming with a nail grooming kit. With an “if it’s good enough for me, it’s good enough for my dog” mindset, pet owners have shown that they’re highly inclined to purchase grooming products for their pets from brands that they trust for their own personal use.

These aforementioned brands, traditionally known for their human products, experienced steep sales declines in beauty and personal care throughout the pandemic. Their pet grooming product lines, however, helped insulate a great deal of those losses and capture growth from an entirely new shopper segment. Beauty and personal care brands looking to enter the pet grooming space will be able to attract pre-existing customers to their pet product lines as they seek out familiar, trusted brands for their furry family members. As the outlook for beauty and personal care remains bleak, moving into pet grooming products can capture additional dollars from DIY-lovers looking to care for their pets at home.

Pet brands need to take advantage of the growth in DIY and get consumers excited about taking care of their pet’s grooming needs at-home. The majority of pet owners have yet to purchase within the pet grooming space, and retailers and brands need to offer easy-to-use, comprehensive product kits that satisfy a variety of grooming needs as consumers familiarize themselves with at-home pet care. In addition, brands and retailers need to teach consumers about the benefits of routine, at-home pet care and make clear connections between their reprioritized sense of self-care and pet care.